I attended a Silicon Valley panel discussion on robotics this evening, and I thought I'd share a summary of the experience.

Rob Lau of "Idea to IPO" (idea-to-ipo.com) opened the seminar by introducing several of the group's members, including Albert Qian of Albert's List. One entrepreneur, Ali, discussed autonomous tutors available 24/7 capable of answering questions immediately. Another member talked about a geolocation service without satellite communication called No GPS.

|

| Food and drinks were available |

Rob provided a quick mission statement. He acknowledged many entrepreneurs are struggling financially, so he ensures his events are affordable to all. His aim is value for our time, which he called our most

valuable asset. His group's global mission is to democratize entrepreneurship, and he referred the audience to his YouTube channel.

I was impressed with Tim Jeghers, the event's videographer. He seemed diligent without being obtrusive.

Eric Hanson of the nationally-recognized WilmerHale law firm moderated, and he did an excellent job, following up when answers were not clear.

I've been a huge fan of WilmerHale ever since Attorney Seth Waxman's oral arguments before the Supreme Court, and I was pleased to be able to visit one of the law firm's offices, even though Mr. Waxman works out of D.C., not Palo Alto.

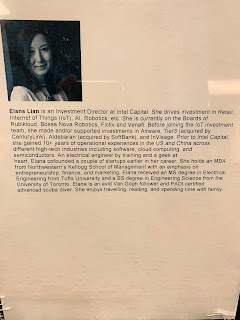

All the panelists were interesting, but I enjoyed Elana Lian's comments the most.

Below is a heavily paraphrased summary of each speaker's comments, which attempts to capture the gist of their opinions.

Elana Lian: I’m with Intel Capital, and I focus on AI and robotics. Opportunity is everywhere. We focus on the B-to-B side. We bring computer vision and the AI to the processing unit, a complex undertaking due to factors like data analysis and different operating systems. One example [of this fusion] is the company Bossa Nova, which makes a robot that scans shelves and QR codes in the retail industry. That involves scanning (robot vision), movement/navigation, and processing.

I agree in the long term, other jobs will replace the ones eliminated by technology, but in the meantime, people recognize short-term challenges, including in media such as Black Mirror.

One of the most critical things is to talk to the end user.

Just because you’re solving a really cool problem doesn’t mean someone will buy it. [My favorite quote of the night.]

Kelly Chen: I’ve always been interested in the quantitative

side. I have an engineering background as well as an MBA. We think about logistics--everything from shipping to

packing. I’m optimistic about this space, because due to software and

reinforcement learning, we can do things in weeks today that took one full year

in 2012. 'Reinforcement learning" is how the robot learns, i.e., the robot uses probabilistic models similar to the human brain rather than machine learning,

which doesn’t allow the robot to perform tasks it hasn’t seen before.

We are also involved in autonomous long-haul trucking. We’re

excited about what this technology can do for the labor market, because few

people want to do long-haul trucking, such as deliveries from the East coast to the West coast. With new technology, however, drivers can stay

closer to home, see their families more often, and focus on handling "last

mile" issues.

We invest on the enterprise side, and

enterprises make decisions based on concrete factors. When selling to

consumers, it’s more emotional, more based on sentiment. From an investment

approach, we tend to be cautious. If you have a demo that works in the lab, it

doesn’t mean it will work in the wild.

|

| National Geographic, 08.2018 |

I think GDPR and data privacy are important, but a security

failure in an autonomous vehicle is much more dangerous than a data breach.

Brandon Reeves: I’m an early stage investor. How do you

reinvent a new cycle in an established business? In the short term, there will

be job displacement because of technology, but if the Industrial Revolution is any indication, more

jobs will be created in the long-term (10, 20, and 50 years from now).

From a funding perspective, with consumer

robotics, the difficulty is that investors want a market

to already exist, while innovators often look ahead to fulfilling a demand that

doesn’t yet exist. In terms of what consumers will accept, a lot of it comes

from the DNA of a company rather than the product itself. We ask, “Do consumers

trust the company?” [Rather than, “Do consumers trust the product?”]

I’m very against co-working spaces at the early stages [of a company or idea].

Re: job displacement, I don’t believe in UBI—I tend to focus on opportunity and

retraining. I also think UBI is against immigrants, because it makes it harder from a policy perspective to increase immigration. I believe immigration has been responsible for America's success, and I don't want to support a policy that will reduce it. The way to increase wages is through productivity

growth, and you get productivity growth through technology. I do worry some

jobs will eventually experience so much productivity growth, they’ll no longer

need human beings, but I’m not sure we can predict the exact timeline.

20% of America's GDP is healthcare or healthcare-related.

Re: a robot tax to mitigate job losses, in general, you don’t want to levy a tax that hurts innovation in the short term,

but the long term is different.

Nuno Goncalves Pedro: I’m a VC investing in next generation

applications focused on the consumer. Our time horizon is five to ten years,

preferably five to seven years.

We don’t believe in the idea that robots need

to be anthropomorphic. A doorbell or an ATM is also a small robot, but for some reason, people will trust a human-looking robot more than a doorbell or an ATM. Why

don’t we have ATMs that look like human beings dispensing money? It’s different

selling to consumers than to businesses, but the patterns in usage between

businesses and individuals are becoming similar. We’re in the midst of a big

shift.

There’s an entrenched supply chain that makes it hard for

newcomers to break through, but even these entrenched systems are missing pieces. At the same time, if

I’m GM or another OEM, why not own my software? Why rely on third parties just

because that’s the way the supply chain is set up?

There’s a war for the home going on right now. Amazon,

Google, Apple are all vying for the home. Facebook tried and failed.

From an ethics perspective, unfortunately, I do think ethics

is in the hands of engineers, and engineers aren’t meant to be thinking about ethics. They’re meant to think about algos and functions. Meanwhile, most CEOs do

not know what their engineers are doing, so there’s a gap between technical

implementations and business leadership.