Marc Lamont Hill succinctly describes the liberal Democratic platform in a single page in Nobody (2016) (paperback, pp. 177):

The problem with this approach is that it ignores government's tendency to borrow, particularly from private banks. If tax revenues and other fees do not match the cost of services, especially when new services are needed, private banks provide the loans/bonds. In short, the "liberal" anti-privatization model renders government at state and local levels dependent on private banks. (It should not be surprising, then, that many have called America's Democratic Party the party of Wall Street, and its Republican Party the party of Big Oil.)

I suppose one could argue "deficits don't matter" and render Congress's power of the purse into a literal money tree, showering all cities and states with interest-free loans. And yet, if governance could be so simple, why not make it even simpler and have Congress give all individuals money directly? Indeed, many have suggested the latter as the basis of UBI (Universal Basic Income), but the experiment has always been directed towards the unemployed or the neglected, perhaps assuming human beings prefer meaningful work over none at all.

We have now arrived at the true difficulty at the intersection of commerce and government: creating meaningful jobs while avoiding excessive and uneven inflation.

Even ignoring, as Mr. Hill does, commerce's complex trade/security agreements with other nations and the trillions of dollars of debt these agreements assume, nowhere in his analysis of commerce does he make room for the ambitious, the persecuted, or the minority not agreeing with his definition of the "common good." And while it is true ambition often paves its way through artifice, there we can find government's true calling: protecting common people from the ambitious while creating an economic system bringing everyone together so as to prevent persecution as well as self-segregation.

The problems of modern commerce are vast and complex, centering chiefly around unimaginative local governments favoring the tried-and-true, leading to uneven development, de facto segregation, then the very inequality Mr. Hill abhors. Private entities are not silver bullets against corruption, but history teaches us any entity suffering from a lack of competition--such as public jails or police departments--will eventually become corrupt or deficient. With respect to privatized jails, we have learned it is possible for the private to become as corrupt as the public without sufficient oversight of necessary adjoining agencies--in this case, ICE and police departments. Finally, if corralling commercial activity were so straightforward as prioritizing the public good over the profit motive, one wonders why the mafia or black markets exist at all.

The first step to strengthening social cohesion is trust in government, which requires not only transparency, but an understanding that modern commerce is so complex, only cooperation at both the neighborhood and national levels will create viable solutions. States like Singapore are small enough to make the gap between neighborhoods and their national Parliament a short walk, while countries like Norway have such small populations, a gap between their capitals and outlying regions can never become too great. America, like Russia and China, possesses none of these advantages and must work harder to prevent a police state from taking over completely in the name of the public good. As an American resident, I am confident most Americans favor the public good, but less so when it comes to the hard work and humility in getting there.

© Matthew Mehdi Rafat (2019)

Bonus I: when academics without a direct understanding of law and economics talk about the "profit motive," almost every criticism as applied to corporations could be applied to the mafia, which operates across borders using the singular method of violence--a tactic corporations cannot use. (Unlike your local loan shark, Wells Fargo or JP Morgan cannot send someone to break your legs if you default or declare bankruptcy.)

Instead, multinational corporations must contend with three or four layers of overlapping jurisdictions, a level of red tape making it easier for governments, whether liberal or conservative, to demand ever-escalating payments, legal fees, or bribes to do business and to bring consumers more choices. When such choices are made without any regard to long-term planning, chaos results, causing critics to blame the profit motive rather than the target government's poor vision. Thus, the better arguments against corporate power revolve around short-termism (i.e., short term profit motives) and lobbyists' efforts to insulate corporations from accountability or transparency (i.e., giving corporations the same qualified immunity as some government agents).

Bonus II: while we're on the topic of overlapping jurisdictions, let's review why such a dynamic exists. First, redundancy. If a local police department is overwhelmed (think riots), it needs to be able to request additional personnel. A local entity prepared for all worst case scenarios will bankrupt local government or deprive cities and counties of much-needed social and other services, eventually guaranteeing a repressive police state. (Mr. Hill himself explains this exact issue in discussing Ferguson, Missouri.)

Second, local entities represent local citizens, who may have different needs and wants than national representatives. By forcing national and multinational participants to adhere to local regulations, cities and counties can shape their own destinies--up to a point. (Justice Louis Brandeis' shorthand term for this interplay is "laboratories of democracy.")

Third, if a local entity is corrupt (think Mississippi Burning (1988)), a local resident has no recourse but to appeal to an outside authority having jurisdiction.

In short, overlapping jurisdictions were not designed to promote complexity for the sake of complexity, serving an unnecessary expansion of law school and academic influence, nor to allow looser federal purse strings to wedge themselves between police departments and local residents.

Bonus III: democracy is hard to successfully implement over long periods of time, and even harder the larger the geographical area. A blue collar worker in Kansas, absent some respected intermediary, may have nothing in common (except language) with a software engineer in California. The idea of a common language is to establish respected intermediaries, such as journalists (think Charles Kuralt, Studs Terkel), to bridge the gap and help form a national identity, but of course language can manufacture social dissolution just as well as social cohesion.

It may be the case that a 5 to 7 days workweek is inimical to a well-functioning democracy by not allowing enough voters sufficient time for study and contemplation. And yet, one can be certain a majority of contemporary American adults, most of whom had ineffective public school teachers, would spend their additional free time on less-than-edifying activities. Is it any wonder, then, that America has become the land of the distracted, home of the vested interests? Why would a minority or immigrant with options choose such a place? And how have less developed areas, which preserve local agency through national neglect or capitol corruption, attained the very character wished upon us by our most educated and most sincere?

The problem with this approach is that it ignores government's tendency to borrow, particularly from private banks. If tax revenues and other fees do not match the cost of services, especially when new services are needed, private banks provide the loans/bonds. In short, the "liberal" anti-privatization model renders government at state and local levels dependent on private banks. (It should not be surprising, then, that many have called America's Democratic Party the party of Wall Street, and its Republican Party the party of Big Oil.)

I suppose one could argue "deficits don't matter" and render Congress's power of the purse into a literal money tree, showering all cities and states with interest-free loans. And yet, if governance could be so simple, why not make it even simpler and have Congress give all individuals money directly? Indeed, many have suggested the latter as the basis of UBI (Universal Basic Income), but the experiment has always been directed towards the unemployed or the neglected, perhaps assuming human beings prefer meaningful work over none at all.

We have now arrived at the true difficulty at the intersection of commerce and government: creating meaningful jobs while avoiding excessive and uneven inflation.

|

| From local Los Altos, California newspaper (June 2019) Every single state executive office is run by Democrats, from Governor to Insurance Commissioner. |

The problems of modern commerce are vast and complex, centering chiefly around unimaginative local governments favoring the tried-and-true, leading to uneven development, de facto segregation, then the very inequality Mr. Hill abhors. Private entities are not silver bullets against corruption, but history teaches us any entity suffering from a lack of competition--such as public jails or police departments--will eventually become corrupt or deficient. With respect to privatized jails, we have learned it is possible for the private to become as corrupt as the public without sufficient oversight of necessary adjoining agencies--in this case, ICE and police departments. Finally, if corralling commercial activity were so straightforward as prioritizing the public good over the profit motive, one wonders why the mafia or black markets exist at all.

The first step to strengthening social cohesion is trust in government, which requires not only transparency, but an understanding that modern commerce is so complex, only cooperation at both the neighborhood and national levels will create viable solutions. States like Singapore are small enough to make the gap between neighborhoods and their national Parliament a short walk, while countries like Norway have such small populations, a gap between their capitals and outlying regions can never become too great. America, like Russia and China, possesses none of these advantages and must work harder to prevent a police state from taking over completely in the name of the public good. As an American resident, I am confident most Americans favor the public good, but less so when it comes to the hard work and humility in getting there.

© Matthew Mehdi Rafat (2019)

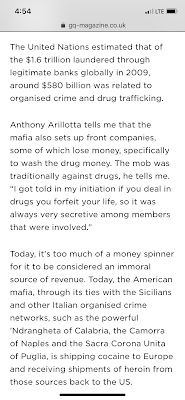

Bonus I: when academics without a direct understanding of law and economics talk about the "profit motive," almost every criticism as applied to corporations could be applied to the mafia, which operates across borders using the singular method of violence--a tactic corporations cannot use. (Unlike your local loan shark, Wells Fargo or JP Morgan cannot send someone to break your legs if you default or declare bankruptcy.)

|

| GQ article by Alex Hannaford (June 2019) |

Bonus II: while we're on the topic of overlapping jurisdictions, let's review why such a dynamic exists. First, redundancy. If a local police department is overwhelmed (think riots), it needs to be able to request additional personnel. A local entity prepared for all worst case scenarios will bankrupt local government or deprive cities and counties of much-needed social and other services, eventually guaranteeing a repressive police state. (Mr. Hill himself explains this exact issue in discussing Ferguson, Missouri.)

Second, local entities represent local citizens, who may have different needs and wants than national representatives. By forcing national and multinational participants to adhere to local regulations, cities and counties can shape their own destinies--up to a point. (Justice Louis Brandeis' shorthand term for this interplay is "laboratories of democracy.")

Third, if a local entity is corrupt (think Mississippi Burning (1988)), a local resident has no recourse but to appeal to an outside authority having jurisdiction.

In short, overlapping jurisdictions were not designed to promote complexity for the sake of complexity, serving an unnecessary expansion of law school and academic influence, nor to allow looser federal purse strings to wedge themselves between police departments and local residents.

Bonus III: democracy is hard to successfully implement over long periods of time, and even harder the larger the geographical area. A blue collar worker in Kansas, absent some respected intermediary, may have nothing in common (except language) with a software engineer in California. The idea of a common language is to establish respected intermediaries, such as journalists (think Charles Kuralt, Studs Terkel), to bridge the gap and help form a national identity, but of course language can manufacture social dissolution just as well as social cohesion.

It may be the case that a 5 to 7 days workweek is inimical to a well-functioning democracy by not allowing enough voters sufficient time for study and contemplation. And yet, one can be certain a majority of contemporary American adults, most of whom had ineffective public school teachers, would spend their additional free time on less-than-edifying activities. Is it any wonder, then, that America has become the land of the distracted, home of the vested interests? Why would a minority or immigrant with options choose such a place? And how have less developed areas, which preserve local agency through national neglect or capitol corruption, attained the very character wished upon us by our most educated and most sincere?